Option 2

Bank Account Input

Option 1

Text to set expectations

Option 3

Banner in Offer Page

Option 4

Link 1 bank account first

Averie

Marketing Manager

Mathilde

Loans Product Manager

Jenna

Full-stack engineer

THE PROBLEM

How might we enable sellers to proactively apply for a loan that suits them best?

1) View

2) Evaluate

3) Select

THE PROBLEM

How might we enable sellers to proactively apply for a loan that suits them best?

Averie

Marketing Manager

Mathilde

Loans Product Manager

Block

During my time at Square, I was the lead designer for the term loans product, while 0 to 1 designing an alpha Line of Credit and Receivables Financing product and working with the International Loans team. Applying my range in design expertise from workshop design to iterative design through A/B testing, I enjoyed designing credit products for sellers to keep their businesses moving forward.

Scaling Design systems

Design workshops

Data-driven design

Product- thinking

A/B testing

The Square Loans product is underwritten through seller eligibility and processing data. We offer two types of loans: flex and term. Flex allows sellers to pay back a percentage of daily sales through their daily processing, while Term, a newer product offering, is paid back in fixed monthly payments, traditional to bank loans. As we introduced more credit products, sellers became confused about their eligibility. I proposed a workshop to help sellers proactively select a loan offer that suits their business best.

Block

During my time at Square, I was the lead designer for the term loans product, while 0 to 1 designing an alpha Line of Credit and Receivables Financing products. Applying my range in design expertise from workshop design to iterative design through A/B testing, I enjoyed designing credit products in the fintech space for sellers to keep their businesses moving forward.

Scaling Design systems

Design workshops

Data-driven design

Product- thinking

A/B testing

Throughout the workshop, I split up cross-functional specialty peers into different teams. Each came up with a concept they articulated in a Concept Design template I created, in which I then converted into the 3 different concept visions above.

Throughout the workshop, I split up cross-functional specialty peers into different teams. Each came up with a concept they articulated in a Concept Design template I created, in which I then converted into the 3 different concept visions above.

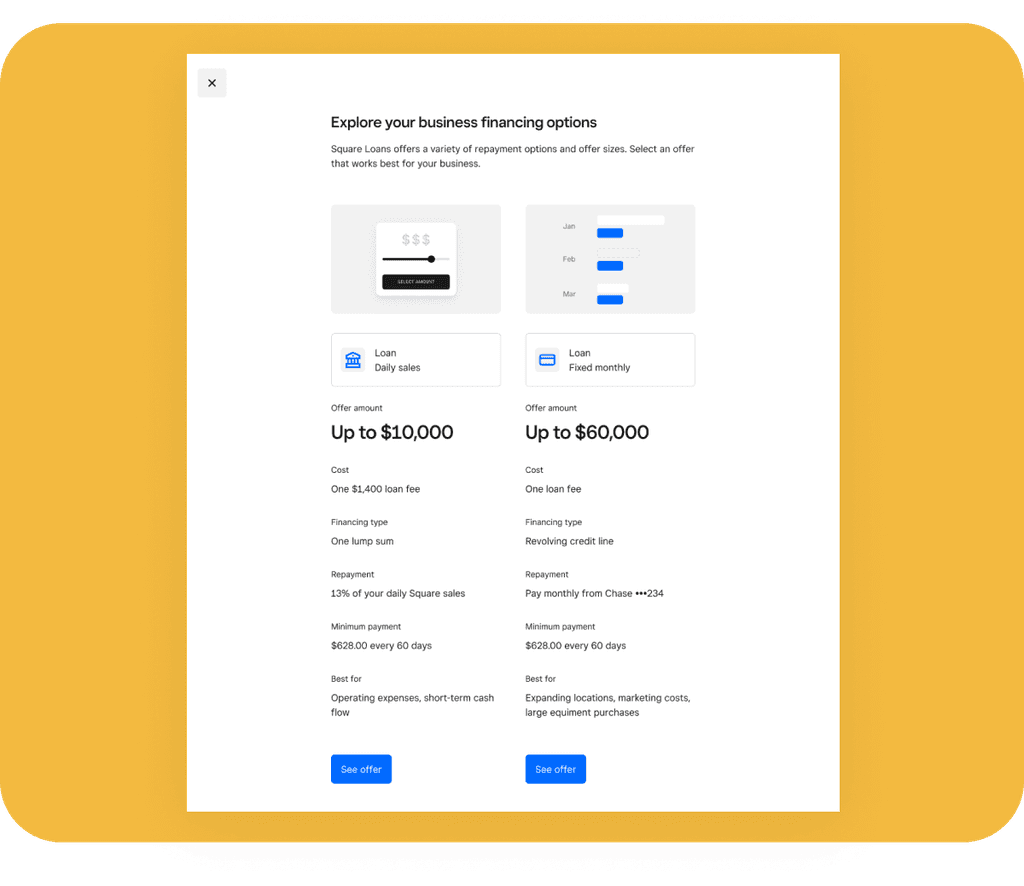

Business Financing Options

Sellers can clearly see the value of both types of loans and how they’re paid back from a high level. Because they are preeligible for both in this product structure, they can see varying loan amounts and fees associated when selecting “See offer”.

Loan Recommendation Wizard

Sellers can clearly see the value of both types of loans and how they’re paid back from a high level. Because they are preeligible for both in this product structure, they can see varying loan amounts and fees associated when selecting “See offer”.

Real-time Loan Offer Comparison

Sellers can adjust the amount they’re looking for, and see how loan variables for flex vs. term are affected.

During the workshop, I divided each specialty into separate groups. Each group brainstormed ideas to observe, consider, and choose a loan, eventually settling on a particular idea they expressed using a Concept Design framework. Subsequently, this was translated into the 3 distinct concept visions displayed above.

Integrating Plaid to yield higher loan offers

Another significant project I worked on during my time at Block was thinking about the UX of collecting external bank account data, via Plaid, in order to provide higher loan offers. This helped expand inventory by lending a more complete view of sellers finances because repayment is not solely tied to future revenue processed through Square, as in existing Flex Loans. Throughout my design process answering the following how might we question, I kept in mind product values I set with the cross-functional team: valuable, consistency, clear, and simplicity.

How can we integrate Plaid (5-6 step experience) into the existing Term Loans product?

Integrating Plaid to yield higher loan offers

Another significant project I worked on during my time at Block was thinking about the UX of collecting external bank account data, via Plaid, in order to provide higher loan offers. Throughout my design process answering the following how might we question, I kept in mind product values I set with the cross-functional team: valuable, consistency, clear, and simplicity.

Integrating Plaid to yield higher loan offers

Another significant project I worked on during my time at Block was thinking about the UX of collecting external bank account Plaid data in order to provide higher loan offers. Since we underwrote loan offers based off of seller processing data, allowing external bank account selection would enable us to provide higher loan offers, which could help sellers expand their businesses. Throughout my design process answering the following how might we question, I kept in mind product values I set with the cross-functional team: valuable, consistency, clear, and simplicity.

How can we integrate Plaid (5-6 step experience) into the existing Term Loans product?

existing Term Loans experience

Integrating Plaid to yield higher loan offers

Another significant project I worked on during my time at Block was thinking about the UX of collecting external bank account Plaid data in order to provide higher loan offers. Since we underwrote loan offers based off of seller processing data, allowing external bank account selection would enable us to provide higher loan offers, which could help sellers expand their businesses. Throughout my design process answering the following how might we question, I kept in mind product values I set with the cross-functional team: valuable, consistency, clear, and simplicity.

Tab button to select how many bank accounts

Sellers typically don't have more than 4 external bank accounts.

Reminder for how many bank accounts linked

Seller can skip linking at any given point.

I led a workshop with cross-functional team members - engineering, marketing, UX writers - to ideate solutions. Knowing 85% of sellers typically take out loans when it aligned with timing for their business (from a survey conducted by the lead user researcher), whether it was the need for a new refrigerator or expanding locations, framing the HMW question around this key insight was crucial. During the workshop, I divided each specialty into separate groups. Each group brainstormed ideas to view, evaluate, and choose a loan, in a mad-libs exercise, eventually settling on a particular idea they expressed using a Concept Design framework. Subsequently, I translated each into the 3 distinct Figma visions displayed below.

Rethinking the credit ecosystem

Business Financing options

Sellers can clearly see the value of both types of loans and how they’re paid back from a high level. Because they are pre-eligible for both in this product solution, they can see varying loan amounts and fees associated when selecting “See offer”.

Business Financing options

Sellers can clearly see the value of both types of loans and how they’re paid back from a high level. Because they are pre-eligible for both in this product solution, they can see varying loan amounts and fees associated when selecting “See offer”.

Loan Recommendation Wizard

Sellers can specify how much they’re looking for, by when and for what, so we can learn how loans are used. And based on their sales, we recommend the best loans product for them.

Loan Recommendation Wizard

Sellers can specify how much they’re looking for, by when and for what, so we can learn how loans are used. And based on their sales, we recommend the best loans product for them.

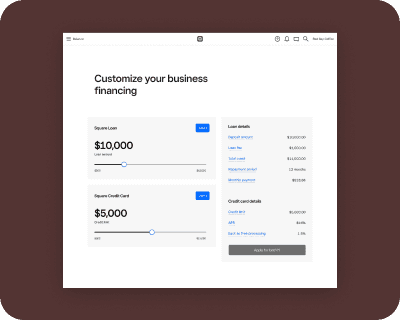

Real-time Loan Offer Comparison

Sellers can adjust the amount they’re looking for, and see how it affects loan variables for flex vs. term.

Real-time Loan Offer Comparison

Sellers can adjust the amount they’re looking for, and see how it affects loan variables for flex vs. term.

Business Financing options

Sellers can clearly see the value of both types of loans and how they’re paid back from a high level. Because they are pre-eligible for both in this product solution, they can see varying loan amounts and fees associated when selecting “See offer”.

Loan Recommendation Wizard

Sellers can specify how much they’re looking for, by when and for what, so we can learn how loans are used. And based on their sales, we recommend the best loans product for them.

Real-time Loan Offer Comparison

Sellers can adjust the amount they’re looking for, and see how it affects loan variables for flex vs. term.

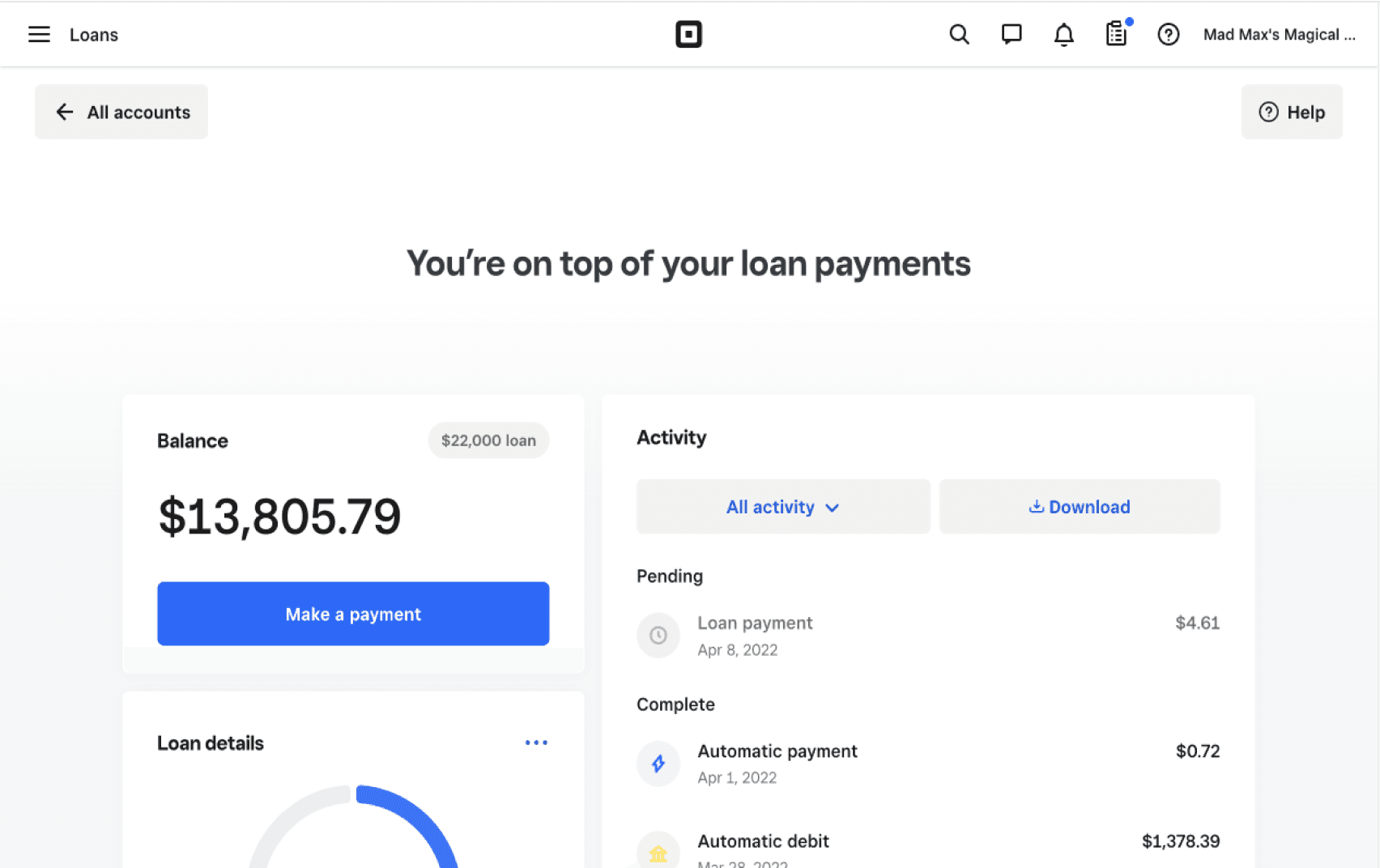

After evaluating each of the user experiences, I concluded on the direction above. Overall, the final design solution yielded impressive results. It contributed to a 48% increase in offer size, for sellers who completed both Plaid and FICO linking. Seller who linked external bank accounts linked an average of 1 bank account, and the UX resulted in a 24% conversion, of sellers who started the Plaid flow, compared to the 14% conversion in the standard term loans flow with FICO only.

Throughout the workshop, I split up cross-functional specialty peers into different teams. Each came up with a concept they articulated in a Concept Design template I created, in which I then converted into the 3 different concept visions above.

Business Financing Options

Sellers can clearly see the value of both types of loans and how they’re paid back from a high level. Because they are preeligible for both in this product structure, they can see varying loan amounts and fees associated when selecting “See offer”.

Loan Recommendation Wizard

Sellers can clearly see the value of both types of loans and how they’re paid back from a high level. Because they are preeligible for both in this product structure, they can see varying loan amounts and fees associated when selecting “See offer”.

Real-time Loan Offer Comparison

Sellers can adjust the amount they’re looking for, and see how loan variables for flex vs. term are affected.

During the workshop, I divided each specialty into separate groups. Each group brainstormed ideas to observe, consider, and choose a loan, eventually settling on a particular idea they expressed using a Concept Design framework. Subsequently, this was translated into the 3 distinct concept visions displayed above.

Business Financing options

Sellers can clearly see the value of both types of loans and how they’re paid back from a high level. Because they are pre-eligible for both in this product solution, they can see varying loan amounts and fees associated when selecting “See offer”.

Loan Recommendation Wizard

Sellers can specify how much they’re looking for, by when and for what, so we can learn how loans are used. And based on their sales, we recommend the best loans product for them.

Real-time Loan Offer Comparison

Sellers can adjust the amount they’re looking for, and see how loan variables for flex vs. term are affected.

THE PROBLEM

How might we enable sellers to proactively apply for a loan that suits them best?

1/ View

2/ Evaluate

3/ Select

THE PROBLEM

How might we enable sellers to proactively apply for a loan that suits them best?

1/ View

2/ Evaluate

3/ Select

Integrating Plaid to yield higher loan offers

Another significant project I worked on during my time at Block was thinking about the UX of collecting external bank account data, via Plaid, in order to provide higher loan offers. This helped expand inventory by lending a more complete view of sellers finances because repayment is not solely tied to future revenue processed through Square, as in existing Flex Loans. Throughout my design process answering the following how might we question, I kept in mind product values I set with the cross-functional team: valuable, consistency, clear, and simplicity.

How can we integrate Plaid (5-6 step experience) into the existing Term Loans product?

Integrating Plaid to yield higher loan offers

Another significant project I worked on during my time at Block was thinking about the UX of collecting external bank account data, via Plaid, in order to provide higher loan offers. This was a significant project that helped expand inventory by lending a more complete view of sellers finances because repayment is not solely tied to future revenue processed through Square, as in existing Flex Loans. Throughout my design process answering the following how might we question, I kept in mind product values I set with the cross-functional team: valuable, consistency, clear, and simplicity.

How can we integrate Plaid (5-6 step experience) into the existing Term Loans product?

Integrating Plaid to yield higher loan offers

Another significant project I worked on during my time at Block was thinking about the UX of collecting external bank account data, via Plaid, in order to provide higher loan offers. This helped expand inventory by lending a more complete view of sellers finances because repayment is not solely tied to future revenue processed through Square, as in existing Flex Loans. Throughout my design process answering the following how might we question, I kept in mind product values I set with the cross-functional team: valuable, consistency, clear, and simplicity.

How can we integrate Plaid (5-6 step experience) into the existing Term Loans product?

THE PROBLEM

How might we enable sellers to proactively apply for a loan that suits them best?

1/ View

2/ Evaluate

3/ Select

After evaluating each of the user experiences, I concluded on the direction above. Overall, the final design solution yielded impressive results. It contributed to a 48% increase in offer size, for sellers who completed both Plaid and FICO linking. Seller who linked external bank accounts linked an average of 1 bank account, and the UX resulted in a 24% conversion, of sellers who started the Plaid flow, compared to the 14% conversion in the standard term loans flow with FICO only.