How many banks do you use for business purposes?

Count the number of banks (e.g. Chase, Wells Fargo) you use to run your business.

1

2

3

4+

This information will be used to improve your loan offers

It won’t be used to reduce or cancel any loan offers

Continue

Skip account linking

Instantly unlock more money for your business

Help us understand your business finances outside of Square to increase your loan offer.

Your pre-approved amount

$65,000

Credit score checked

You unlocked an extra $50,000

Bank account linked

You unlocked an extra $5,000

Link a bank account

Your bank info will only be used to improve future loan offers

5% more

View offer

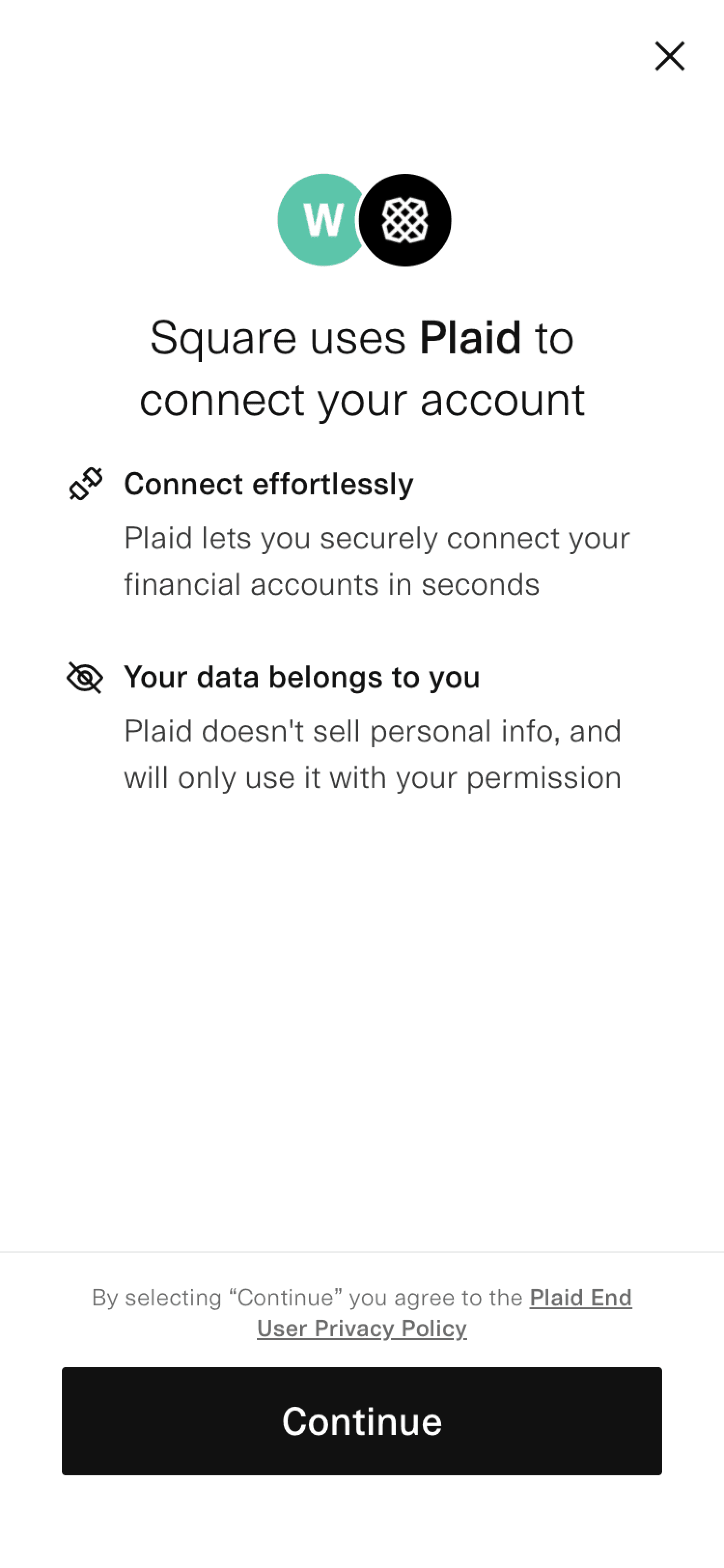

The Plaid Product Experience

Plaid offers a distinct user experience to collect external bank account information. We wanted to ensure we maintained transparency, simplicity, and clarity in the product experience. Thinking about a framework for linking financial information overall was fundamental to the Plaid Integration project, especially as we introduce more linking functionality to scale.

Banner in Loan Offer

In this solution, I explored a flow where sellers initially link just one bank account, with the option to add more on the loan offer page. Since we didn’t know how many external accounts a seller might have, we also needed to define the technical constraints for when to stop displaying the banner prompting them to link additional accounts.

Incentive per Link Type

As we explored a scalable solution for linking external seller information, it was important to account for the incentives tied to each link type. In this solution, I introduced an education screen to communicate that linking data—such as FICO scores, bank accounts, and future data sources—can increase a seller’s loan offer. Prior research showed that sellers are motivated by larger loan amounts, as well as benefits like reduced fees and extended repayment timelines. To encourage linking, we tied each data point to a potential increase in loan offers, making the value of linking more tangible.

Copy to Incentivize Sellers

In this solution, I used strategic copy to both incentivize sellers and clarify how their external bank account information would be used. The phrase “More money, the merrier” served as a friendly nudge, encouraging sellers to link as many bank accounts as possible to maximize their potential loan offer.

Solution

Choose your own Adventure

Eventually, we concluded on the "Choose your own Adventure" solution, where upmarket sellers can input the number of bank accounts they have, and the product experience holds the seller accountable for linking the number they mentioned initially. The bank account education screen duals as an opportunity to remind sellers how we use their bank account information, as we hypothesized this design decision balances seller trust with a seamless loan experience.